The management functions related to planning and control of financial resources in an institute is known as financial management.

The main goal of financial management is to maximize the business related value (wealth) of the proprietors of the business.

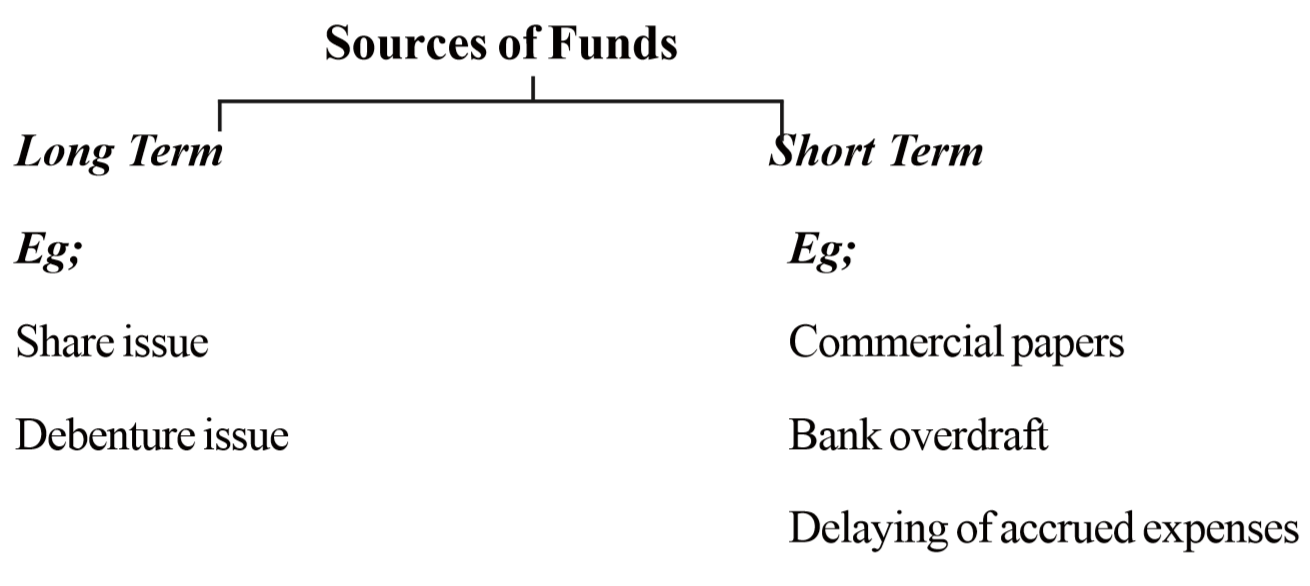

Sources of funds can be classified on various criteria

As internally and externally

As direct and indirect

As direct and indirect

Two types of vital decisions are made in financial management:

Investment decisions

Financing decisions

Investment decisions

Decisions made to invest funds in fixed assets and current assets are investment decisions.

Financing decisions

Decisions regarding how to provide the funds for investing in fixed and current assets are financing decisions.

Cash budget

The cash budget is prepared considering the expected cash receipts and cash payments in a particular future period.

Cash budget can be identified as an internal financial estimate used in planning and decision making.

Uses of preparing a cash budget:

Ability to make effective cash investments, if any future cash excess can be identified in advance

Ability to prepare for possible cash shortages successfully in any future shortage can be identified in advance

Facilitating planning and control of cash by comparing with actual cash transactions

Capital budget

Planning to invest the funds currently available in a business in long term assets or long term projects with the purpose of gaining future benefits is known as capital budgetting.

Capital budgetting decisions made by the finance manager are known as long term investment decisions.

Eg;

Constructing a new building with the purpose of expanding business affairs.

Purchasing a new machine.

Long term expenses incurred for advertising programmes.