Influencing the cost of debts and liquidity by changing interest rates and money supply is called monetary policy.

Quantitative and qualitative monetary instruments are the two main instruments used to operate the monetary policy.

Quantitative credit control instruments are the common methods of reducing the supply of loans. The volume of loans and the direction of the flow of the loans are controlled by the qualitative credit control instruments.

Quantitative monetary instruments are of three types such as Bank interest rate, statutory reserve ratio and open market operations.

Policy interest rates are:

Bank interest rate.

Repurchasing rate.

Reselling rate.

Among them repurchasing rate and reselling rate are used in the open market operations.

Qualitative credit control instruments are of various types:

Credit Ceilings

Collateral requirements for loans

Selective interest rates

Moral suasion

The independent body that was set-up to carry out the monetary policy of Sri Lanka is the Central Bank Of Sri Lanka.

The mission of the Central Bank is to maintain economic and price stability and the stability of the monetary system for sustainable economic development through policies, supervision, commitment and excellence.

Following are the dual objectives of the Central Bank:

To maintain economic and price stability

To maintain the stability of the monetary system.

Economic and price stability means maintenance of a low level of inflation.

Price Stability is important in order to:

Promote economic growth

Distribute resources efficiently

Minimize risks to producers, consumers and investors

Make economic planning successfully

Creating an effective monitoring framework and strong and protective payment and settlement system for depositors and investors are the infrastructure facilities needed to materialize stability of the monetary system.

Stability of monetary system is important for the following reasons:

To make financial institutions and market function effectively

To avoid balance of payment crises

To finalize the price of assets

To protect market liquidity

The process of regulating monetary instruments to influence the interest rate and money supply to reach the objectives of economic and price stability and the stability of monetary policy is monetary policy.

The targets of regulating the monetary policy can be shown as follows:

Operational target – Amount of high powered money

Intermediate target – Interest and money supply

Final Target – Stability of the monetary system

The special, very strong and prominent monetary institutions that act as financial intermediaries in the monetary system with profit motive are called commercial banks.

Services provided by Commercial banks

Accepting deposits

Providing loans

Long term loans

Short term loans

Services as an agent

Common Utility services

Assisting in foreign banking activities

Providing pawning services

Providing safe keeping services

Providing related services in foreign currency transactions

Objectives of Commercial bank

To maintain liquidity

To maintain profitability

Statutory reserve ratio

According to the regulations of the Central Bank, commercial banks must maintain a certain percentage of its deposits as a reserve. This ratio is known as the statutory reserve ratio.

The Central Bank changes this ratio from time to time.

Excess Reserves

The amount of reserves exceeding the statutory requirement is called excess reserves.

Excess reserve = Current money reserve – Statutory reserve.

Excess reserve is determined based on the following factors:

The demand for loans

Selection of commercial banks between liquidity and profitability

Monetary policies of the Central Bank

Deposit Multiplier

Deposit multiplier is the number of times of expansion of deposit or creation of credit with a demand deposit.

Deposit multiplier is equal to the reciprocal of statutory reserve ratio.

Liquidity – Profitability

When liquidity is maintained profitability decreases and when profitability is maintained, liquidity decreases.

Since there is a clash between the two objectives, mentioned above, assets should be maintained in a balanced manner.

Credit Creation

Generating more deposits than the existing deposits by lending the excess reserves of commercial banks is called Credit creation.

Since only one bank functions in a monopolistic banking system, credit creation is possible. But it is impossible for a single bank in a banking system to create money.

The credit creation of the commercial banking system is based on the following assumptions:

After making the initial deposit there is no inflow or outflow of money in the banking system

All the borrowers deposit their total amount of loans in another commercial bank

No bank maintains excess reserves

There are limitations to credit creation as follows:

If people prefer to retain money with them, excess reserves of commercial banks will decline

Credit creation decreases when banks prefer to maintain excess reserves

Decreasing the demand for loans

Classifies the financial system of Sri Lanka as below:

Banking sector

Central Bank of Sri Lanka.

Licensed commercial banks

Licensed specialized banks

Other depository financial institutions

Registered financial companies

Co-operative rural banks

Thrift and Credit Co-op Societies.

Other special finance institutions

Special leasing companies

Primary dealers.

Merchant banks

Financial Brokers

Unit Trusts

Venture Capital Investment Companies

Credit Rating Institutions

Accorded savings institutions

Insurance companies

Employee provident funds

Employee trust funds

Other provident funds

Government services provident funds

The total money stock that circulates among the general public at a given period is called money supply.

Money supply is a stock concept.

The items of monetary aggregates which are bank liabilities can be categorized as follows:

Base money / High powered money / Reserve money supply

Narrow money supply

Broad money supply

Broad money concept can be categorized again as:

M1= Narrow money supply

M2= Broad money supply

M2b= Consolidated broad money supply

M4 =Very broad money supply

Base money can be analyzed in two ways:

Using Central Bank liabilities

Using Central Bank Assets

Determinants of base money supply:

Net lending to the government by the Central Bank

Net foreign assets of the Central Bank

Other net assets of the Central Bank

Lending to commercial banks by the Central Bank

Components of high powered money:

Notes and coins in circulation

Deposits of commercial banks with the Central Bank

Deposits of government institutions with the Central Bank

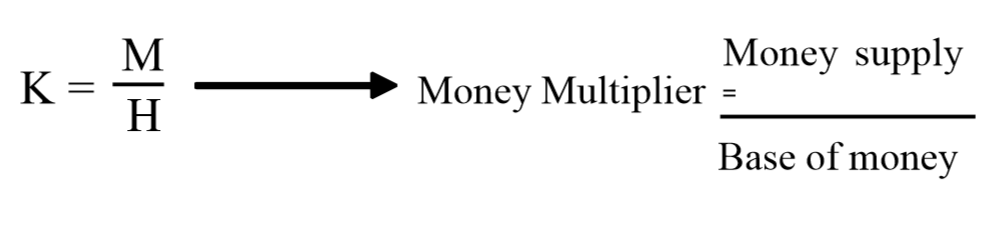

Money Multiplier

Money multiplier is the ratio between money supply and high powered money.

Therefore multiplication of high powered money and money multiplier is the money supply.

The relationship of money supply, high powered money, and money multiplier can be shown by the following equations.

The preference of the people to keep money in the form of money at a given time can be defined as demand for money.

Demand for money is based on the following three main factors.

Transaction motive

Precautionary motive

Speculative motive

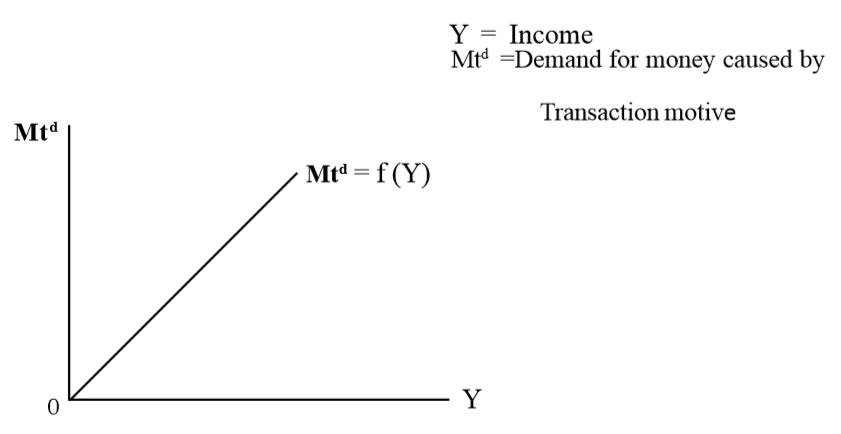

Transaction Motive

Since there is a gap between receiving income and spending the income by a person holding money balances for transactions is called demand for money on transaction motive.

Demand for money on a transaction motive basically depends on the income level of people.

There is a positive relationship between the income level and demand for money on transaction motive.

It can be shown by a function and a graph as below:

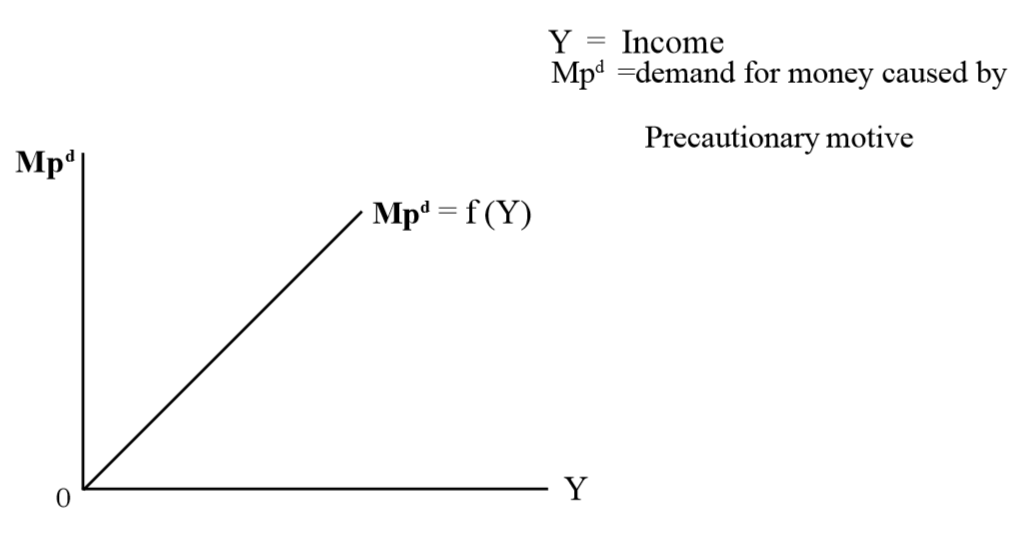

Precautionary Motive

Holding money balances to spend in unexpected situations is known as demand for money on precautionary motive.

Demand for money on precautionary motive also depends on the income level of people.

There is a positive relationship between the income and the demand for money on precautionary motive.

It can be shown by a function and a graph as below:

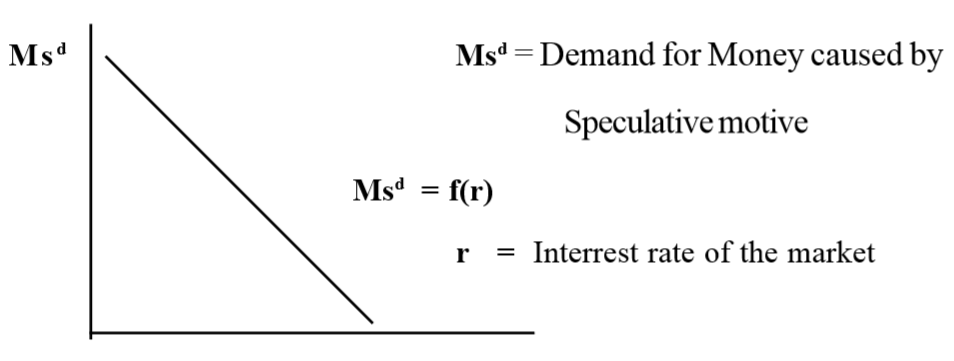

Speculative Motive

Demand for money to earn profits in future from investments is called the demand for money on speculative motive.

There is a negative (inverse) relationship between the demand for money on speculative motive and interest rates.

It can be shown by a function and a graph as below:

Anything that is generally accepted as a medium of exchange can be considered as money.

Characteristics of Good money

Acceptability

Durability

Uniformity

Divisibility

Portability

Stability of value

Discourages forgery

Currency

Money which is legally accepted for transactions within the country is Currency.

Bank Money

Current accounts with commercial banks are Bank money.

Modern Money

Currencies and cheques are introduced as Modern money.

Near Money

Assets that can be converted to a medium of exchange easily are Near money.

Money Substitutes

Money Substitutes act as a temporary medium of exchange but they do not comply with the function of money as a store of value.

Electronic Money

Electronic money is a method of transaction through software storing the value of physical money electronically.

Functions of Money

As a medium of exchange.

As a store of value.

As a unit of account.

As a medium of deferred payment.

Internal value of Money

The Internal value of money is the quantity of goods and services that can be purchased by a unit of money of that country.

The Internal value of money is determined on the domestic price level.

External value of Money

The External value of money is the quantity of goods and services that can be purchased by a one unit of money of that country from another country.

The External value of money is determined on the exchange rate.

Inflation brings about various economic effects.

Decline in the real value of money has adverse effects on fixed income earners, depositors and creditors.

Variable income earners and debtors are benefited by inflation.

Real income can be calculated using the following formula:

Economic cost of inflation is the decline in efficiency of economic activities.

Monetary policies and monetary policy management can be used to control inflation.